When a deposit arrives earlier or later than expected, it is often due to payment processing issues, not missing money or benefit cuts. Processing timing can change at several points between the sender, payment networks, and banks. This article explains the legitimate reasons deposit timing shifts, how processing works behind the scenes, and why agencies like the Social Security Administration and banks may show different posting times even when payments are sent on schedule.

What Are Payment Processing Issues

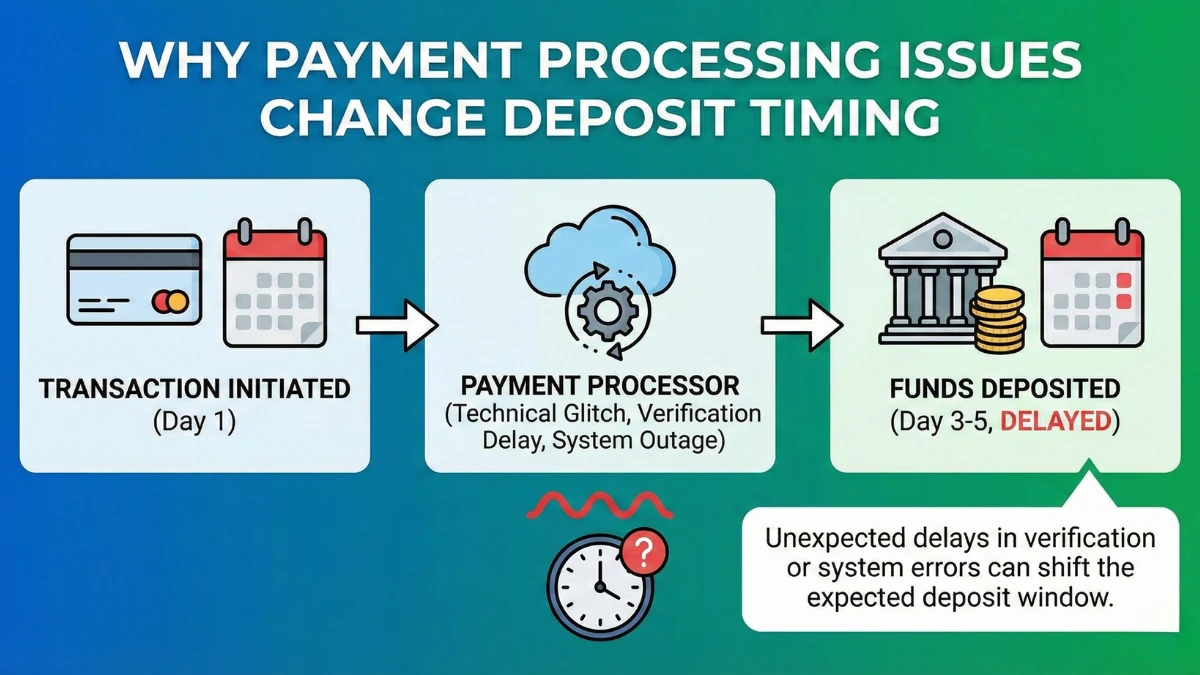

Payment processing issues refer to technical, verification, or timing steps that occur after a payment is released but before it posts to a recipient’s account. These steps are routine and exist to ensure accuracy, security, and compliance.

Common Reasons Deposit Timing Changes

| Cause | What Happens |

|---|---|

| Bank processing cut-off times | Deposits post next business day |

| Weekend or holiday processing | Payments shift earlier or later |

| Verification checks | Temporary hold before posting |

| Payment network delays | Settlement timing changes |

| Account status issues | Deposit queued or returned |

Bank Cut-Off Times Matter

Banks process deposits in batches. If a payment arrives after a bank’s daily cut-off, it may post the following business day even though it was sent on time.

Weekends and Federal Holidays

Most payment systems do not settle on weekends or holidays. When a scheduled date falls on a non-business day, deposits may post earlier or on the next business day, depending on the sender’s rules.

Verification and Security Reviews

Automated security checks can briefly hold deposits for fraud prevention or identity verification. These holds usually resolve quickly and do not change the payment amount.

Payment Network Settlement Timing

Electronic payments move through clearing networks before reaching banks. Congestion or routine maintenance can cause minor settlement delays that shift posting times.

Account-Specific Issues

Closed accounts, name mismatches, or recent account changes can cause deposits to be queued or returned, requiring correction before reposting.

What Has Not Changed

There is no new rule causing random delays, no reduction in payment amounts, and no penalty tied to processing timing. These shifts occur under long-standing banking and payment system rules.

What Recipients Should Do

Allow one business day for posting, check bank notifications, and verify account details. Contact the sender only if a deposit is not received after the adjusted business window.

Key Facts

- Processing timing can shift deposits without affecting amounts

- Bank cut-off times are a common cause

- Holidays and weekends change posting dates

- Verification holds are usually temporary

- Most issues resolve automatically

Conclusion

Deposit timing changes are usually the result of normal payment processing steps, not missing payments or policy changes. Understanding how banks and payment networks work helps set realistic expectations and avoid unnecessary concern.

Disclaimer

This article is for informational purposes only and does not constitute financial or legal advice. Payment posting times depend on banking systems and official processing rules.